124 /

“Get Your $shit In Order” is a slide I put up during my talk on the business of photography aka #freelancelife. I usually say that unless you’ve got a trust fund, are independently wealthy, or have a partner who has a great job and you don’t really need to work… One of my best pieces of advice is to start saving now.

And don’t ever stop.

So, here’s my talk in a nutshell:

If you’re still in school, take a business class or two. If not, audit one.

Talk to a CPA and a financial planner. My CPA is worth every penny.

Set yourself up a business - S-corp or LLC. A CPA can advise what’s best.

Set up a 401k (SEP, Roth, and/or traditional IRA) and start saving now.

Only about 10% of my job is making pictures. The other 90% is running a small business. Everything I do for my business, I consider the ROI (return on investment). I ask: will spending money now (on marketing and promos, a personal project, or a trip to NYC to meet with editors) pay off in the future? If not, it’s tougher to justify spending it.

I’m also a proponent of Suze Orman’s 8-month Emergency Fund. The pandemic highlighted the need; sadly, I learned many friends didn’t have one.

Automate money: 30% of every check gets put away for taxes, for retirement, for buying gear in the future, for taking vacations, for my emergency fund, etc.

“It’s not how much money you make, it’s how much money you save.”

— one brilliant piece of advice I got when starting out

So why am I saying all this? I’m having more and more of these conversations with friends, with people dropping into my DMs, and photographers contacting me for consulting advice on business-related stuff.

Caroline Yang, a great commercial and editorial photographer in Minneapolis, who’s around my age, recently told me, “…lately when I meet with young photogs, at the end I always ask if I can also give them a piece of life advice: INVEST EARLY. Even if it’s just a little bit—but start saving early because later down the line it will be harder.” PREACH.

Another friend, Brittany Greeson, who’s 31, and has been freelancing full-time since 2016, recently sent me her budget and asked where she could make cuts, how she could maximize her savings, and how to get her money working for her. I walked through honest numbers on that spreadsheet with her, and we’ve had some frank conversations about the industry and the need to diversify revenue streams (more corporate and commercial, less editorial). I love that she’s thinking about this early. I love that she started contributing to a Roth IRA about 4 years ago, I love that she’s planning for her future now.

It’s a real conversation we should be having more of, especially as freelancers. The realities of this industry are scary sometimes. We need to talk about money.

As freelancers, we have to prepare for when times are lean. Here in DC, that is summer — August is worst of all because Congress is not in session, editors are on family vacations, and my bank account starts that slow roll backward. But I know this is coming every year. And I can prepare for it, so while it hurts, it doesn’t sting quite as badly. And it’s like a friend said in that pull quote above: “It’s not how much we make, it’s how much we save.”

But as a freelancer, the other bonus of financial independence is freedom. It’s being able to say no to bad assignments, toxic editors, and horrible contracts. It’s feeling like you have control and ownership over your work, and thus your life.

So this year, I decided to try something new. Strict minimalism. That’s an oversimplification, but, essentially, as a New Year’s resolution, I decided to stop spending money on unnecessary stuff, and keep track of that spending.

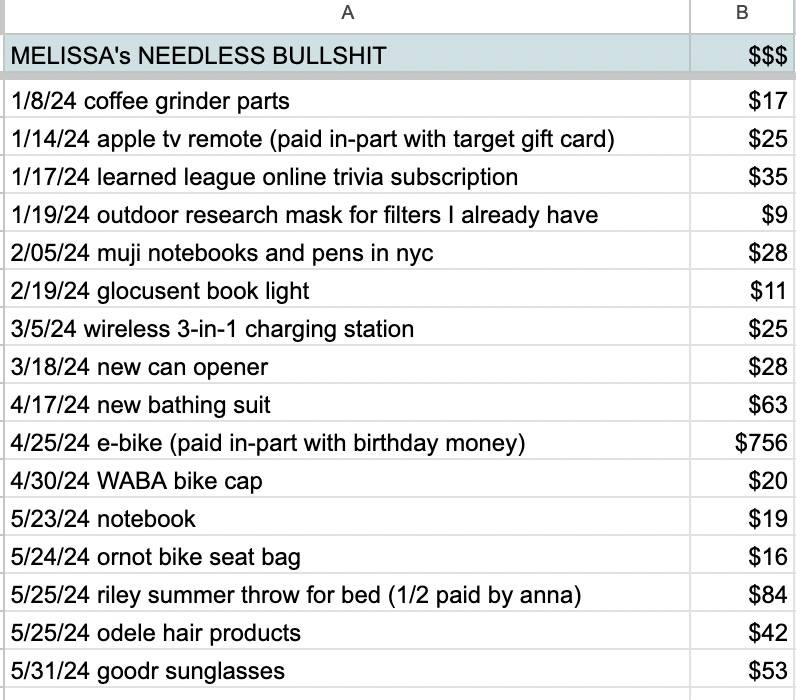

If you’re interested, here’s my “2024 wants not needs” as the spreadsheet is called.

(Yes, I bought an e-bike, that was a huge want, and about half of this year’s “needless spending” but again ROI was considered… saving gas, having more fun. Plus, we have one car, and I wanted a grocery-getter/errand-running bike. So I used the money I got for my birthday this year, plus some serious savings [Rakuten, Retail Me Not, Honey — all of which I have set up as browser extensions!] found online to get it for about half price. I’m writing this Substack from a coffee shop I rode my e-bike to!).

This was partly a challenge issued to a friend, (who shall remain nameless), who has complained to me for years about money. He’s making more than he’s ever made, but like a lot of us who didn’t grow up with a lot of money, he’s also spending more than ever before. With his first big paycheck, he bought a fancy Aeron chair for his office. Why, because he could, he told himself he deserved it. It symbolized that he’d made it. And I get it. But damn is it damaging long term.

I’d also love to see him retire when he wants to, take his family on vacation, and be able to weather an emergency without stress. I’d love to see him not have credit card debt — compounding, exponentially. I’d love to see him not freak out if the phone doesn’t ring for a week, or a month, or more. I’d love for him to be thinking about the future, instead of just the short term.

I’d post his list of needless shit too, but sadly he decided not to play along. He hasn’t posted a single entry. He justifies most of his purchases as things he absolutely must have and convinces himself he needs. That’s the wrong mindset (to me). I need to plan for my future, that’s what I need. Because nobody else will.

I’ll end this with a few tips and things to think about, things that have worked for me (and friends), but also with the caveat that I’m not a professional, so do your homework and do what works best for you.

I’ll keep harping on Suze Orman’s 8-month emergency fund. It’s a must.

Set up a budget. Know where your money is going and WHY.

High-Yield Savings Accounts (HYSA) - Getting 5% interest on checking is sweet. I’m not sure why I didn’t do this earlier, but I’m sure glad I have it now.

Automate your savings. Automatically have money taken out of each check, most banks have this feature on their websites, so you don’t even have to think about it. Automate for special things, too, like putting $20/week into a special savings account for tickets to Mexico to see a World Cup game in 2026.

Get into the habit of ALWAYS paying off your credit cards each month. 20%+ interest will get you in the hole real fast. One good rule of thumb is don’t put it on the credit card if you can’t afford to pay it off immediately. (Read up on snowball vs avalanche methods!)

Speaking of credit cards though, I love playing the travel hack game. I buy things with my credit cards that I can pay off immediately, solely to get points and miles. As a freelancer, it’s how I pay for my vacations (I have a Delta Amex business card, a Marriott Bonvoy card, and a Chase card with a decent travel portal and solid points to Apple products conversion rates).

$hit happens. If you currently have a lot of money sitting on credit cards, collecting high interest each month, this should be your primary focus. start looking into 0% balance transfer cards and be good about paying it off by the time the intro period ends.

The sooner you open a 401k, the more interest you’re compounding. (One friend said: I often felt embarrassed or ashamed for not knowing more about investing—and I believe that alone can be very paralyzing. It can make it easy to think, oh I’ll figure this out later—-until it’s 10 years later and you’ve lost all of that potential compound interest! I do think all of the financial professionals taking it to social media makes it more accessible. And I bet the shame and embarrassment are an obstacle for many—especially in our industry when we already don’t make much! )

If you have a great year freelancing, think about contributing to a SEP IRA first. You can contribute up to 25% of your net earnings from self-employment. It lowers what you make on paper, so you can lower your taxes that year. That money, when in mutual or index funds will make more than a HYSA.

Live below your means. But by all means, LIVE.

Prioritize where your money goes and be smart about what you can cut and how you can save (Rocket Money helps you find unwanted subscriptions you have). Maybe you don’t need Hulu, Netflix and/or HBO Max, you can use Kanopy for free and put that money toward paying down a credit card or into a savings account dog-eared for something special. Your money should help support what you want out of life, your politics, your values, etc... So, if you want to travel more, make that a goal. If you believe in donating to charities, set up a Daffy account or set aside money for that. If you want to be better about reducing your carbon footprint, cancel that Amazon Prime membership and buy used (Facebook marketplace and Buy Nothing groups are where my son’s toys come from).

I’ll end with a fun metaphor Brittany Greeson shared with me recently: Your career is a house and having your shit together financially is the absolute foundation. Sure you can have a gorgeous mansion but if the foundation has cracks it’s all going to cave in one day. If you have a simple log cabin on a solid foundation, you’ll have something more timeless.

Damn. This was amazing

Practical and sound advice. Thank you for sharing! Emergency fund is key- used mine up during the pandemic then replenished it when I had a job. Using it again while I'm in-between.